The insurance crisis in the construction sector was quite widespread 2021 and also spread to other sectors including accountancy and legal.

Architects, Engineers and Surveyors all saw a significant increase in their insurance costs and greater cover restrictions, as insurance market capacity reduced and more insurance companies announce their withdrawal from the professional indemnity market.

We recommend the link to this guide is also circulated to all Partners, Directors and Senior Managers for their general awareness as well as for risk management purposes.

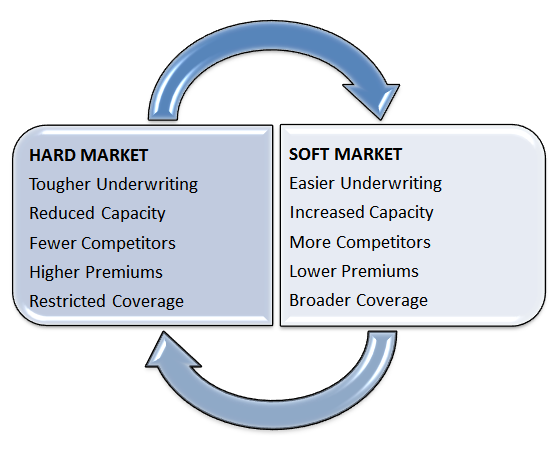

What caused the 'hard' insurance market?

The insurance market is normally highly competitive or 'soft' for periods of typically 15 years. Over this long period, market rates drop eventually below profitable levels as insurers aggressively compete against each other for their market share, driving premiums down.

Against this reduction, the total volume of claims being notified continues to grow in size and numbers, eventually becoming unsustainable to the point that a significant market adjustment is necessary - a 'hard' market.

It was widely reported that the insurance cost of the Grenfell tragedy was the trigger for the last market adjustment when markets feared more major claims relating to cladding and construction. As a result of their fears, many loss-making insurers withdrew from the market, allowing those remaining insurers to apply more restrictive cover and vastly increase their rates.

The Coronavirus pandemic added to the insurance market's concern as a wave of new insurance claims relating to covid were anticipated.

How long does it last?

How long does it last?

The insurance market moves in a cycle between 'soft' and 'hard' conditions. After a comparatively brief period of hardening it always eventually returns to the 'soft' and highly competitive climate again.

This is normally impossible to predict, but past experience shows that the hard market does not last long. When insurance rates return to a high level which the insurance market regards as satisfactory, insurers are attracted back into the market and the competition begins once again.

The hard market may last several years, but there should then follow a long period of intense competition once again when rates fall year on year.

What can you do about it?

In reality, there is nothing you can do to change the force of a harder insurance market but there is a lot a business can do to at least minimise the impact. Read our guidance points below;

- A good impression

- Risk management in a pandemic or similar event

- Know your broker

- Specify your deadline

- Review the level of cover

- Meet your underwriter

- Explaining claims and reserves

- Competition

- Buying online

Create the right impression

Create the right impression

When you complete your proposal form, it will be reviewed by an experienced Underwriter. The completed form is a 'presentation' of your business to the insurance market, so spend some time making sure it looks professional.

Scruffy handwriting or unanswered questions will all go against your business. They will also review your website and cross refer the information online against the information on your proposal form. They use all of this information to judge the quality of your firm.

Risk management and COVID-19

If you spend time and money on risk management and improving quality, make sure your insurer knows about it. This could easily be overlooked and not reflected in your premium so you may want to add some notes on this subject.

A plan managing the risks arising from a pandemic or similar event is important as prudent insurance underwriters are now requesting detailed information on what firms have done to minimise these additional risks.

Know your broker

Get to know your broker, it's important to have a good relationship. They are on your side, so ask your broker for their view of the current PI market for your profession (e.g. have market rates changed since last year) and their plan for managing your renewal. This should be done at least two months before your renewal date so that you can avoid any last-minute premium increase or cover problems.

Specify your deadline

Aim to have your renewal terms and alternative quotations available at least one month before your renewal date. Within reason, ensure that timings for the renewal process are pre-agreed and clearly understood by everyone, especially your broker.

Review your level of cover

Insurance rates rise and fall and so a flexible approach to the level of cover purchased may be necessary sometimes. Instruct your broker to obtain a range of limits so that cost and risk can be fully considered, giving yourself the option to adjust your level of cover up or down as necessary within budget. However, always keep in mind that professional indemnity insurance is 'Claims Made' insurance.

Meet your underwriter

For larger policyholders, meeting your underwriter can have a very positive effect on your insurance cover. This can be set up by a good broker and will help establish a stronger long-term relationship with your Insurer. We encourage underwriter meetings for our larger clients.

Explain any claim payments or reserves

Explain any claim payments or reserves

If you have any claim payments or reserves on your record, don’t rely on a standard print out sheet to give the underwriter a satisfactory explanation. Give some background about the claim and some assurance on the actions taken to avoid a recurrence. If the underwriter isn't given the full story, they will simply apply a negative view and load up your premium or decline to quote.

Create competition

Getting an alternative quotation is an easy process and competition will often result in premiums falling dramatically. Your broker should be one of your most trusted advisers but still needs to be tested sometimes if you want to avoid complacency.

Buy online

Only suitable for very small contractors and businesses, buying professional indemnity insurance online is becoming an easy and effective way of arranging insurance. It has a clear cost advantage to insurers which is passed on to the policyholder. Generally best suited for businesses up to £ 150,000 turnover and with no adverse underwriting features.

For more information about this subject or a discussion with one of our experts, please call us on 0345 251 4000.

This guidance note is intended for information purposes only. It is not and does not purport to be legal advice or specific insurance advice. Whilst all care was taken to ensure its accuracy at the time of writing it is not to be regarded as a substitute for specific advice. If you require specific advice, please contact your brokers or call us on 0345 251 4000. This guidance note shall not be reproduced in any form without our prior permission. © All copyright is owned by Professional Indemnity Insurance Brokers Ltd.